President Asif Ali Zardari has officially granted presidential assent to the Finance Act 2026, enacting the federal budget into statutory law. Effective July 1, 2026, these comprehensive tax overhauls fundamentally transition Pakistan’s fiscal landscape toward automated digital enforcement, extensive data documentation, and standardized cross-matching.

For corporate entities, salaried professionals, and high-net-worth individuals, navigating these finalized statutory changes is vital to maintaining operational compliance and avoiding sudden enforcement measures like localized audit flags or automatic registration suspensions.

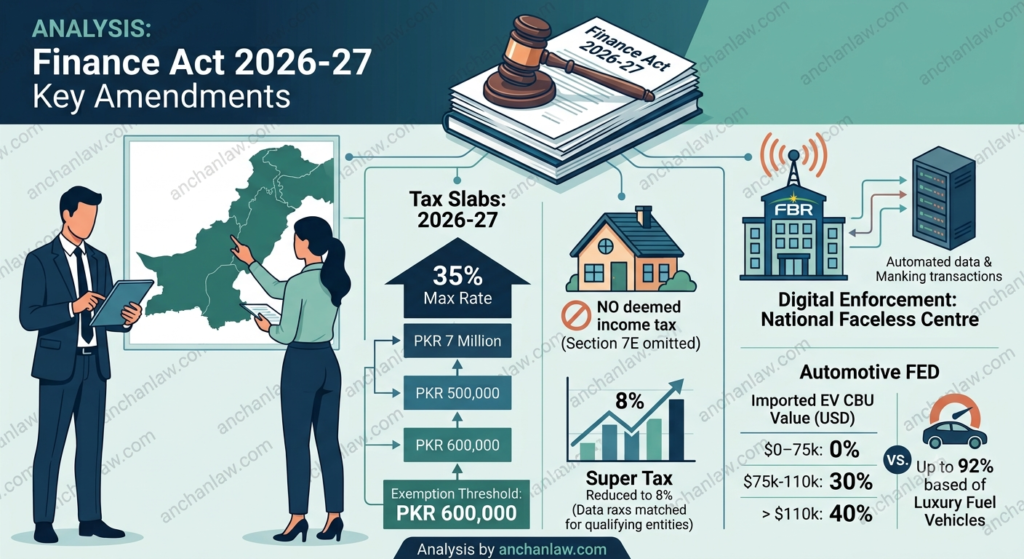

1. Enacted Income Tax Slabs & Direct Tax Structuring

The direct tax framework establishes higher thresholds for upper-tier tax brackets while structurally modernizing penalties, exemptions, and withholding mechanisms.

New Salaried & Individual Tax Slabs (Tax Year 2027)

The final progressive tax slabs for salaried individuals offer broader middle-tier bands while restructuring top-tier limits:

Exemption Threshold: Income up to PKR 600,000 remains completely exempt from income tax (0% rate).

Maximum Tax Bracket: Capped at 35%, triggering only when taxable income exceeds PKR 7 million (providing a significantly wider buffer than the historical PKR 4.1 million threshold).

Surcharge Withdrawal: The controversial 9% surcharge previously applied to high-salaried individual brackets has been completely abolished.

Super Tax & Deemed Income Revisions

Omission of Section 7E (Deemed Income): Following definitive constitutional litigation regarding federal legislative bounds over immovable property, the tax on deemed income from un-utilized immovable property has been permanently omitted. Taxpayers are liable only for actual, realized income streams.

Super Tax Rationalization: The scope of the Super Tax has been narrowed. Individuals or entities earning up to PKR 500 million are entirely exempt. For income exceeding PKR 500 million, the rate is reduced from 10% to 8% (with key banking, oil & gas, and fertilizer sectors retaining their specific sector caps).

Export-Oriented Exclusions: Companies where export revenues comprise more than 80% of total annual turnover are structurally protected from the Super Tax net.

Digital Media & Platform Adjustments

Social Media Withholding Tax: A formalized 5% Withholding Tax (WHT) targets income generated via digital monetization, localized e-commerce networks, and international social media platforms. Banking channels and payment gateways are statutorily mandated to automatically withhold this tax on outbound or inward remittances routed to content creators or non-resident digital platforms.

Fixed Tax Opt-Out: Taxpayers with an annual turnover under Rs200 million may explicitly opt out of the fixed tax regime, provided they file a final, irrevocable declaration certificate with the Tax Commissioner before submitting their returns for Tax Year 2027.

2. Sales Tax, Customs, & Indirect Tax Re-Engineering

Indirect tax laws have been extensively optimized, eliminating broad exemptions and replacing them with integrated system-based pricing firewalls.

Expansion of the Third Schedule (Retail Price Tax)

The application of the standard 18% sales tax levied directly at source on retail packaging (under the Third Schedule of the Sales Tax Act, 1990) has been expanded to encompass primary consumer lines:

Edible oils, commercial sauces, and confectionery.

Footwear, sanitary ware, cosmetics, household utensils, and ceramic products.

Integration Incentive: Targeted sales tax concessions are legally preserved for footwear manufacturers and retail entities who achieve complete integration with the FBR’s real-time Point-of-Sale (PoS) digital networks.

Distribution Margins & Sectoral Exemptions

Minimum Tax for Distributors: The minimum tax rate applied to distributors across 14 core commodity sectors—including Fast-Moving Consumer Goods (FMCG), pharmaceuticals, fertilizers, dairy products, sugar, and packaged foods—is statutory capped at 0.5%.

Aviation Inclusions: The sales tax exemption on the import or lease of aircraft, corporate jets, and corresponding spare parts has been universally leveled to include all domestic airlines operating within Pakistan.

Special Regimes: For steel melters, re-rollers, and composite industrial units, sales tax collection is now determined on the basis of per-unit electricity consumed, formulated via an FBR-notified minimum price benchmark.

Automotive & EV Federal Excise Duty (FED)

The Federal Excise Duty structure for imported Electric Vehicles (EVs) and SUVs in completely built units (CBU) has transitioned entirely to a US Dollar valuation model:

Vehicle Valuation (USD)Enacted FED RateUp to $75,0000% FED$75,000 to $110,00030% FEDAbove $110,00040% FED

High-Capacity Combustion Engines: Traditional fuel-combustion luxury vehicles face steep FED escalations, fixed at 86% for engines between 2000cc and 3000cc, and hitting 92% for luxury vehicles exceeding 3000cc.

3. Statutory Enforcement, Faceless Administration, & Corporate Safeguards

The core operational pivot of the Finance Act 2026 is the elimination of discretionary physical tax oversight in favor of machine-driven compliance firewalls.

The National Faceless Centre & Centralized Data

Faceless Audits: Assessment proceedings, comprehensive audits, and initial appellate functions are moving entirely to the electronic, identity-concealed National Faceless Centre to prevent direct personal interaction between taxpayers and Inland Revenue officers.

Banking Repository Integration: The State Bank of Pakistan (SBP) is legally empowered to construct a centralized digital transactional repository. This allows the FBR to algorithmically cross-match high-value financial movements against an individual’s unique identifiers and declared income profiles.

E-Invoicing & Supply Chain Firewalls: Top-tier manufacturers must integrate directly with real-time electronic invoicing platforms. Non-compliance triggers immediate automated registration suspension. Furthermore, the FBR will host a live public register of fake invoice issuers; input tax credits will be summarily denied to any business purchasing from these flagged entities.

Enhanced Procedural Safeguards for Taxpayers

To guard against arbitrary executive action under these newly automated systems, the Act secures vital legal defenses for corporate taxpayers:

Pre-Notice Audit Report Requirements: The FBR is legally barred from issuing a recovery show-cause notice without first providing a detailed Audit Report. Taxpayers have a mandatory 15-day statutory window to file written legal objections against the findings or the nominated audit team.

Slashed Limitation Period: The limitation period allowed for reopening past, historical tax assessments has been reduced from 10 years down to 5 years, offering corporate entities significantly faster legal finality.

Corporate Tax Advisory & Legal Compliance

Adapting corporate frameworks to meet the digital reporting mandates, e-invoicing integrations, and realaligned direct tax provisions of the Finance Act 2026 requires specialized statutory oversight. For restructuring compliance mechanisms, contesting arbitrary audit selections, or representing matters before the appellate forums, reach out to secure dedicated counsel.

Schedule a Professional Consultation

Navigating the newly enforced provisions, digital audit frameworks, and corporate compliance mandates of the Finance Act 2026 requires proactive statutory oversight. Whether you need to restructure your corporate tax framework, contest an arbitrary FBR audit selection before appellate forums, or manage high-stakes M&A compliance, our firm provides the dedicated legal counsel your business demands. Contact Anchan Law today to secure strategic advisory services tailored to your operational objectives.

Office Location: Islamabad, Pakistan